The selling of Life Insurance Policies to the British Home Children

(page incomplete -more information to be added)

.from the dictionary of cdn biography LIFE INSURACE re george cox

Aside from occasional troubles brought on by dips in the business cycle, most of the Cox companies prospered handsomely during the Laurier years. Their business methods came under close scrutiny by the federal royal commission appointed in 1906 to investigate the Canadian life-insurance industry. Its proceedings revealed substantial cross-trading, subsidization, and other insider exchanges among Canada Life, Imperial Life, and other Cox family firms; some of these transactions were covert and/or technically illegal. The commissioners concluded, in their Report of 1907, that Cox’s absolute control of Canada Life had “to a marked extent influenced the investments of the company, which have been made to serve not only the interests of the Canada Life Assurance Company, but also his own interests. . . . In many of these transactions the conflict of Mr. Cox’s interest with his duty is so apparent that the care of the insurance funds could not always have been the sole consideration.”

Aside from occasional troubles brought on by dips in the business cycle, most of the Cox companies prospered handsomely during the Laurier years. Their business methods came under close scrutiny by the federal royal commission appointed in 1906 to investigate the Canadian life-insurance industry. Its proceedings revealed substantial cross-trading, subsidization, and other insider exchanges among Canada Life, Imperial Life, and other Cox family firms; some of these transactions were covert and/or technically illegal. The commissioners concluded, in their Report of 1907, that Cox’s absolute control of Canada Life had “to a marked extent influenced the investments of the company, which have been made to serve not only the interests of the Canada Life Assurance Company, but also his own interests. . . . In many of these transactions the conflict of Mr. Cox’s interest with his duty is so apparent that the care of the insurance funds could not always have been the sole consideration.”

Mentions of Life Insurance for the BHC in the Ups & Downs Magazines

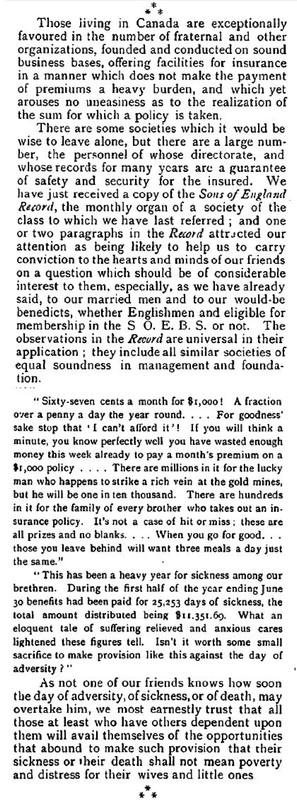

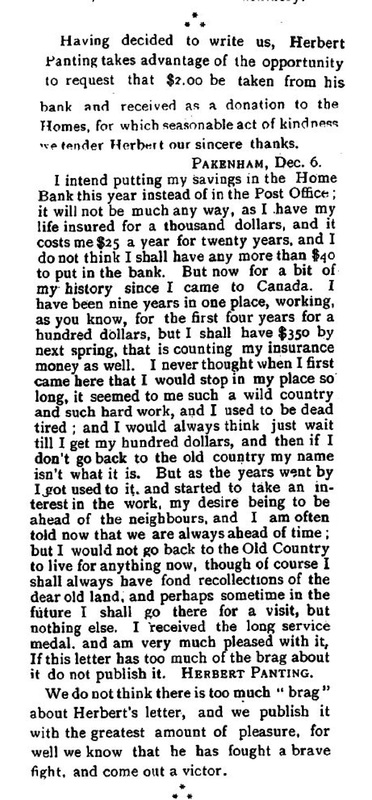

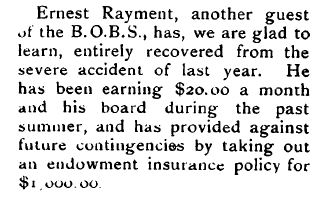

Names mentioned in these clips: Alfred Bush, Tom Vival, Herbert Painting, Ernest Rayment, Frederick A Hanks,

It is god to hear that there was someone, (Kelso) eventually,

in a place of authority acknowledged and spoke against the practice. In the report is it clear how 'child' is defined? The way I read Kelso is that his 'children' includes those under sixteen or fourteen, of any age really, down into the age-range younger than the law would permit a person to enter into an insurance contract of his own making. The parent, or foster parent, or employer or guardian would have to do it. Once the child comes of age and can take a policy out himself (after age 16?) there is sure a vulnerable period when a visitor, say, who is also selling insurance can exert influence both in advising the young person to take a policy, and in the naming of the beneficiary. If the newly insured does not have any family -- that he knows about anyways -- why not name the Home, or the loved Visitor, or the founder of the Home. The stories that Ups and Downs presents as dutiful paradigms of young Barnardo men who have taken out policies, around 1900 and in 1913, have done so in favour of the Home. This is an important point and it provides a reason for not telling children about the existence of siblings. Doing so provides competition for those contending to become the beneficiary. It also, sadly, makes the young person more valuable (to someone or something) dead than alive. And there is the rub of a conflict of interest: that those charged with the protection of the child can come to benefit from his injury. I notice Gillian Wagner has 2-3 pages on Margaret Bondfield and the report she participated in making. In 'Children of the Empire' the recommendation that the emigration of children under under 14 be stopped is presented as the main element, and the several 'minor' recommendations, of which your insurance is one, are alluded to but not described. It is implied too that Bondfield was a Labour MP, and even in the Cabinet of a short-lived Labour Government of Labour led coalition. I think it pays today to look carefully and with an open mind at what organized labour in Canada, for example in the person of DJ O'Donoghue, had to say about child immigration. He and his Toronto Trades and Labor Council had a combatative and bristling relationship with Barnardo's and their agent Owen. When O'Donoghue spoke at the Child Saving Conference in 1894 (it is quoted in Wagner and Bagnell I think) he said something to the effect that there were more than a few ex-Barnardo boys who were in the unions then, and that the tales they told of their indentureships were enough 'to make an ordinary Christian's blood curdle.' Of course it is implied: not so a child saving evangelical Christian's. |

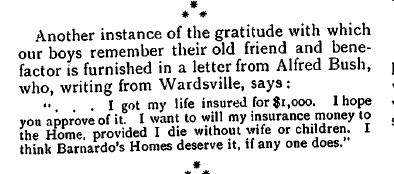

From: brian rolfe <[email protected]> Subject: [BHC] Bondfield Report and Life insurance. Date: Mon, 13 May 2002 17:54:25 -0700 (PDT) Dear List, Here is the passage in my version (RG7 G21 vol. 309 File No. 26) of the Report dealing with life insurance. We found that the representative of an insurance company hed been allowed by one or two of the Societies to approach the boys, whilst in the Receiving Home, on the subject of insuring their lives. In another case an insurance agent had obtained from the Receiving Home a list of boys and their addresses and had visited them on the farms for the same purpose. In a large number of cases it appeared that the boys had actually taken out endowment policies of 1,000 dollars payable at age 40, the annual premiums varying from 17 to 20 dollars. We discussed this question with the Societies concerned, but were not convinced of the desirability of the Societies' representatives associating themselves with the activities of insurance agents, and by so doing influencing the boys to take out policies. It seems to us that boys of this age are not competent to form an opinion for themselves as to the merits of a policy of this kind, that they are liable to misjudge their ability to continue the anual payments, which in many cases would absorb the whole of the balance of their annual wages, and that, in result, a large number of lapsed policies would result. ................... My comment, after ee cummings: There were so many who were so eager to genuflect before the belly of wealth without asking how many children dangled from his watchchain. Brian Rolfe |

From: "Brian Rolfe" <[email protected]>

Subject: Barnardo's and Life Insurance

Date: Tue, 01 May 2001 09:22:09 -0400

Dear List

This posting is about what the Liverpool series (and 1 later issue) of Ups

and Downs tells us about Barnardo's Homes and life insuarance. It is my

conjecture that the Homes derived a significant portion of its funds from

the sale of, and the benefits received from, life insurance.

===========================================

From Ups and Downs, April 1900.

Fred. A. Hanks had written for advice as to joining a friendly society. The

assessment system of beneficiary insurance was explained to him, and the

Sons of England Benefit Society recommended to join. Incidentally his

memotry was jogged in respect to an evanescent umbrella he had borrowed and

was still borrowing. Some of these days a philosopher will arise who will

explain why umbrellas and books are regarded as common property, and then,

knowing the reason, we can govern ourselves accordingly. The following

letter is a pleasing sequel to the foregoing, recognizing, as it does, on

the part of Fred, a desire to leave something more than a good name behind

him, and nominating the Homes as his beneficiary in case of death :

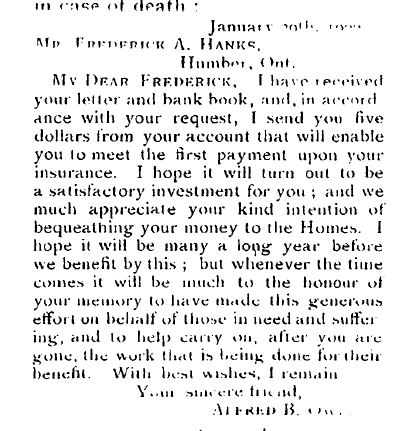

Mr Frederick A Hanks, Humber, Ont

Jan 29 1900

My Dear Frederick: I have received your letter and bank book, and in

accordance with your request, I send you $5 from your account that will

enable you to meet the first payment upon your insurance. I hope it will

turn out to be a satisfactory investment for you; and we much appreciate

your kind intention of bequeathing your money to the Homes. I hope it will

be many a long year before we benefit by this; but whenever the time comes

it will be much to the honour of your memory to have made this generous

effort on behalf of those in need and suffering, and to help carry on, after

you are gone, the work that is being done for their benefit. With best

wishes, I remain,

Your sincere friend,

Alfred B Owen.

===========================================

Ups and Downs May 1913.

"It gives us great pleasure to reproduce the report handed in by Mr Copping

after his visit to Frederick Leslie in January last. Mr Copping writes:

"In view of Frederick's age I had not proposed to call upon him, however,

praised in the surrounding country, I visited this fine young fellow, and

found him in receipt of $200 per annum, with several hundred dollars in the

bank, a teetotaler and non-smoker, thoroughly contented with his lot and

winning enthusiastic praise from members of the family with whom he resides.

A leading characteristic of this young agriculturist is the gratitude he

feels toward the Institution that has cared for him; and he incidentally

mentioned that he has insured his life for $1000 and on the policy indicated

that the money is to be paid to Dr. Barnardo's Homes."

=====================================================

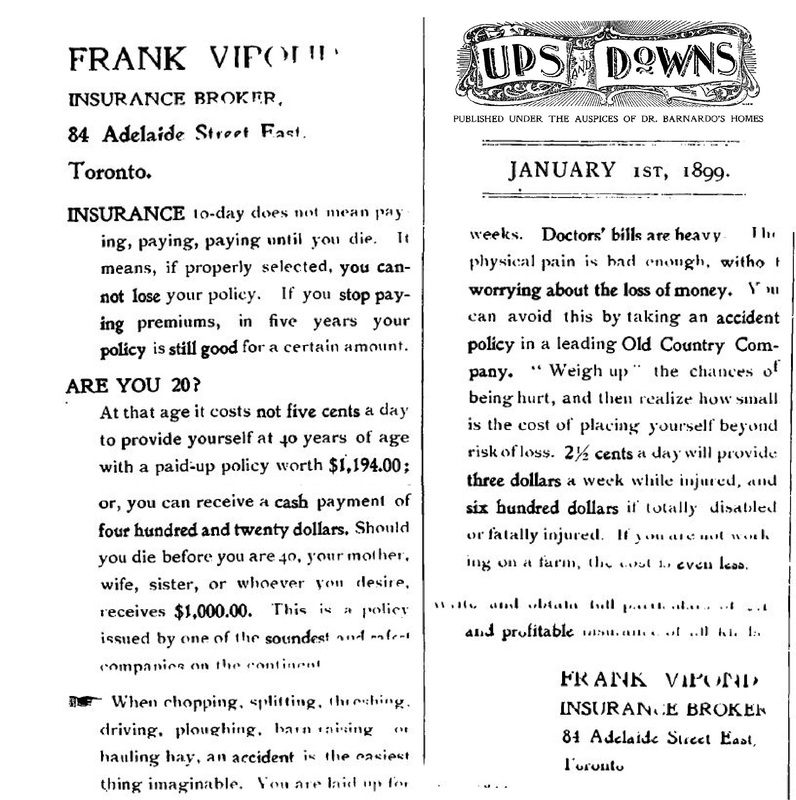

Ups and Downs January 1899.

There is a half-page ad on the inside back cover that reads as follows:

FRANK VIPOND

INSURANCE BROKER

84 Adelaide Street East,

Toronto.

INSURANCE to-day does not mean paying, paying, paying until you die. It

means, if properly selected, you cannot lose your policy. If you stop paying

premiums, in five years your policy is still good for a certain amount.

ARE YOU 20?

At that age it costs not Five cent a day to provide yourself at 40 years of

age with a paid-up policy worth $1194.00; or you can receive a cash payment

of four hundred and twenty dollars. Should you die before you are 40, your

mother, wife, sister, or whoever you desire, receives $1000. This is a

policy issued by one of the soundest and safest companies on the continent.

When chopping, splitting, threshing, driving, ploughing, barn-raising, or

hauling hay, an accident is the easiest thing imaginable. You are laid up

for weeks. <[bold] Doctors' bills are heavy.[end-bold]> The physical pain is

bad enough, <without worrying about the loss of money.> You can avoid this

by taking an accident policy in a leading old country company. 'Weigh up'

the chances of being hurt,and then realize how small is the cost of placing

yourself beyond risk of loss. 2 1/2 cents a day will provide three dollars a

week while injured, and six hundred dollars if totally disabled or fatally

injured. If you are not working on a farm the cost is even less.

Write and obtain full particulars of safe and profitable insurance of all

kinds.

FRANK VIPOND

INSURANCE BROKER,

84 Adelaide Street East,

Toronto.

======================================================

Ups and Downs, April 1903, p 104.

TO EVERY READER.

"The one quality which makes for the success of a young man than any

other is Persistence. This is cultivated more directly and systematically

through regular payments of premiums on a Life Policy than in any other way.

Your special attention is directed to an article on that subject, on

page 53 in this issue. In reading this article bear in mind that every

advantage and privilegementioned may be obtained in the policies of the

Canada Life Assurance Company.

The Canada Life wrote more paid-for business in Canada in 1902 than any

other native company, and its total business in force in Canada is more than

twice as large as that of any other Canadian Life office.

These two facts indicate that Canada Life contracts are up-to- date and

attractive to new insurers, and that the profit returns on old policies are

highly satisfactory to their holders."

=======================================================================

Ups and Downs April 1903.

Page 74. "We had a call at the Home not long ago from William Thomas, who

reported that he had lately arrived from the North-West, where for some time

previous he had been employed on the McLeod Branch of the CPR. Having met

with an accident in the company's employ, he was given three month's

holiday, which he was spending in Ontario. William was anxious to obtain the

address of his sister, as he is carrying insurance policies to the amount of

$6,000.00, of which she is the beneficiary. He has bought land in the

district of Dauphin...."

=================================================

Barnardo Old Boys' Society.

This group was born in the period and in about 1905 it became, or spawned, a

Benefit Society, the BOBBS. Unfortunately the Liverpool series end too soon

to gather much about the BOBBS (it seems to have disappeared, at least from

the pages of Ups and Downs, by 1913) but there are reports of meetings of

the BOBS attended regularly by Frank Vipond.

===============================

Frank Vipond was the managing editor of Ups and Downs in its first 2-3 years

(1895 and 1896) when his official connection with the home was severed,

according to an AB Owen editorial. Nevertheless he contributed a piece to

the October 1901 issue ("The Barnardo Boy," a seven page essay calling on

the grown boys to band together and stand up and be seen; that is, promoting

membership in the BOBS.) and was at least an occasional, and probably a

regular, visitor at meetings of the BOBS. In his life he seems to have worn

a few hats: in the Toronto directory he is in 1899 a journalist, in 1905 a

rep for the 'News', in 1910 Rev Frank Vipond is rector at St Barnabas

Church, Sarah St.

Kenneth Bagnall calls him a champion of the Barnardo cause, and describes

him as a Methodist minister. But from Vipond's advertisement in the 1899

issue one might want to add: insurance broker.

==========================================

With the long illness and decline of Dr Thomas Barnardo preceding for years

his death in 1905, and with the Boer War drawing funds that might otherwise

have continued to flow to the homes, new sources of funding had to be found.

Barnardo's had been founder-dependant: Thomas Barnardo's charisma and his

passionate pleas for money drew donations from wealthy Britons and the man

on the street alike, and his decline and inability to work to the old levels

of energy left the source of their money in question. But in the event

Barnardo's Homes Canadian Branch survived because the grown chidren became

to a significant degree its support. Their duty - to repay the Home that had

helped them when in need - was spelled out in the magazine, and not only

donations but life insurance benefits were solicited by the Homes.

The magazine had years to instill the lesson in its readers, once the

pattern was established, if the youngsters followed the moral teaching of

the anecdotes selected by the editor as fit for printing. The 'need' for

life insurance, even for single men, labourers, just starting out in life,

was established in the readers by repetition of anecdotes of grown boys who

were dutifully repaying what the Home did for them by naming the Home as

beneficiary of whole-life policies.

So far as the insurance companies, Canada Life Assurance among them, were

concerned, Barnardo's Homes were a sales drive waiting to happen: imagine

the opportunity: one man, ABO speaks, and hundreds of his wards line up to

buy. The Institution bred children not only to become self-sufficient, but

also to become good providers in sustaining the work of the Home for the new

generation of immigrant children coming along.

=============================

After a few years of reading about the models presented as the ones to be

emulated, the younger children must have become thoroughly indoctrinated as

to the young adult that they were expected to become: pious, teetotaling and

non-smoking, thrifty savers, hard workers and self-teachers as well as good

students, sober obedient and, in addition, young adults mindful of what the

Homes have done to help them and willing to repay them through donations and

through life insurance benefits.

And it is my opinion that the practices of Barnardo's then, around the

pitching of whole-life policies to young adult men (who worked frequently at

dangerous occupations) has consequences to this day as to what information

Barnardo's Aftercare is willing to release about the brothers of our

Barnardo grandparents.

It is relevant to this question of life insurance that George Albertus Cox,

of Peterborough until ~1888, was president of Canada Life Assurance Company

for many years, and its Peterborough agent before that, from 1861 forward.

It is he who bestowed Hazel Brae on the Home. I have seen him described as

the richest Canadian west of Montreal; and that there is much mystery

surrounding his affairs because his family destroyed almost all of his

papers soon after his death in 1914.

Also of interest is that there was a Royal commission on Insurance in 1907,

and a Royal Commission on Business Practices in 1914, which apparently

resulted in the forced separation of banking, trust and insurance companies.

Brian Rolfe

Subject: Barnardo's and Life Insurance

Date: Tue, 01 May 2001 09:22:09 -0400

Dear List

This posting is about what the Liverpool series (and 1 later issue) of Ups

and Downs tells us about Barnardo's Homes and life insuarance. It is my

conjecture that the Homes derived a significant portion of its funds from

the sale of, and the benefits received from, life insurance.

===========================================

From Ups and Downs, April 1900.

Fred. A. Hanks had written for advice as to joining a friendly society. The

assessment system of beneficiary insurance was explained to him, and the

Sons of England Benefit Society recommended to join. Incidentally his

memotry was jogged in respect to an evanescent umbrella he had borrowed and

was still borrowing. Some of these days a philosopher will arise who will

explain why umbrellas and books are regarded as common property, and then,

knowing the reason, we can govern ourselves accordingly. The following

letter is a pleasing sequel to the foregoing, recognizing, as it does, on

the part of Fred, a desire to leave something more than a good name behind

him, and nominating the Homes as his beneficiary in case of death :

Mr Frederick A Hanks, Humber, Ont

Jan 29 1900

My Dear Frederick: I have received your letter and bank book, and in

accordance with your request, I send you $5 from your account that will

enable you to meet the first payment upon your insurance. I hope it will

turn out to be a satisfactory investment for you; and we much appreciate

your kind intention of bequeathing your money to the Homes. I hope it will

be many a long year before we benefit by this; but whenever the time comes

it will be much to the honour of your memory to have made this generous

effort on behalf of those in need and suffering, and to help carry on, after

you are gone, the work that is being done for their benefit. With best

wishes, I remain,

Your sincere friend,

Alfred B Owen.

===========================================

Ups and Downs May 1913.

"It gives us great pleasure to reproduce the report handed in by Mr Copping

after his visit to Frederick Leslie in January last. Mr Copping writes:

"In view of Frederick's age I had not proposed to call upon him, however,

praised in the surrounding country, I visited this fine young fellow, and

found him in receipt of $200 per annum, with several hundred dollars in the

bank, a teetotaler and non-smoker, thoroughly contented with his lot and

winning enthusiastic praise from members of the family with whom he resides.

A leading characteristic of this young agriculturist is the gratitude he

feels toward the Institution that has cared for him; and he incidentally

mentioned that he has insured his life for $1000 and on the policy indicated

that the money is to be paid to Dr. Barnardo's Homes."

=====================================================

Ups and Downs January 1899.

There is a half-page ad on the inside back cover that reads as follows:

FRANK VIPOND

INSURANCE BROKER

84 Adelaide Street East,

Toronto.

INSURANCE to-day does not mean paying, paying, paying until you die. It

means, if properly selected, you cannot lose your policy. If you stop paying

premiums, in five years your policy is still good for a certain amount.

ARE YOU 20?

At that age it costs not Five cent a day to provide yourself at 40 years of

age with a paid-up policy worth $1194.00; or you can receive a cash payment

of four hundred and twenty dollars. Should you die before you are 40, your

mother, wife, sister, or whoever you desire, receives $1000. This is a

policy issued by one of the soundest and safest companies on the continent.

When chopping, splitting, threshing, driving, ploughing, barn-raising, or

hauling hay, an accident is the easiest thing imaginable. You are laid up

for weeks. <[bold] Doctors' bills are heavy.[end-bold]> The physical pain is

bad enough, <without worrying about the loss of money.> You can avoid this

by taking an accident policy in a leading old country company. 'Weigh up'

the chances of being hurt,and then realize how small is the cost of placing

yourself beyond risk of loss. 2 1/2 cents a day will provide three dollars a

week while injured, and six hundred dollars if totally disabled or fatally

injured. If you are not working on a farm the cost is even less.

Write and obtain full particulars of safe and profitable insurance of all

kinds.

FRANK VIPOND

INSURANCE BROKER,

84 Adelaide Street East,

Toronto.

======================================================

Ups and Downs, April 1903, p 104.

TO EVERY READER.

"The one quality which makes for the success of a young man than any

other is Persistence. This is cultivated more directly and systematically

through regular payments of premiums on a Life Policy than in any other way.

Your special attention is directed to an article on that subject, on

page 53 in this issue. In reading this article bear in mind that every

advantage and privilegementioned may be obtained in the policies of the

Canada Life Assurance Company.

The Canada Life wrote more paid-for business in Canada in 1902 than any

other native company, and its total business in force in Canada is more than

twice as large as that of any other Canadian Life office.

These two facts indicate that Canada Life contracts are up-to- date and

attractive to new insurers, and that the profit returns on old policies are

highly satisfactory to their holders."

=======================================================================

Ups and Downs April 1903.

Page 74. "We had a call at the Home not long ago from William Thomas, who

reported that he had lately arrived from the North-West, where for some time

previous he had been employed on the McLeod Branch of the CPR. Having met

with an accident in the company's employ, he was given three month's

holiday, which he was spending in Ontario. William was anxious to obtain the

address of his sister, as he is carrying insurance policies to the amount of

$6,000.00, of which she is the beneficiary. He has bought land in the

district of Dauphin...."

=================================================

Barnardo Old Boys' Society.

This group was born in the period and in about 1905 it became, or spawned, a

Benefit Society, the BOBBS. Unfortunately the Liverpool series end too soon

to gather much about the BOBBS (it seems to have disappeared, at least from

the pages of Ups and Downs, by 1913) but there are reports of meetings of

the BOBS attended regularly by Frank Vipond.

===============================

Frank Vipond was the managing editor of Ups and Downs in its first 2-3 years

(1895 and 1896) when his official connection with the home was severed,

according to an AB Owen editorial. Nevertheless he contributed a piece to

the October 1901 issue ("The Barnardo Boy," a seven page essay calling on

the grown boys to band together and stand up and be seen; that is, promoting

membership in the BOBS.) and was at least an occasional, and probably a

regular, visitor at meetings of the BOBS. In his life he seems to have worn

a few hats: in the Toronto directory he is in 1899 a journalist, in 1905 a

rep for the 'News', in 1910 Rev Frank Vipond is rector at St Barnabas

Church, Sarah St.

Kenneth Bagnall calls him a champion of the Barnardo cause, and describes

him as a Methodist minister. But from Vipond's advertisement in the 1899

issue one might want to add: insurance broker.

==========================================

With the long illness and decline of Dr Thomas Barnardo preceding for years

his death in 1905, and with the Boer War drawing funds that might otherwise

have continued to flow to the homes, new sources of funding had to be found.

Barnardo's had been founder-dependant: Thomas Barnardo's charisma and his

passionate pleas for money drew donations from wealthy Britons and the man

on the street alike, and his decline and inability to work to the old levels

of energy left the source of their money in question. But in the event

Barnardo's Homes Canadian Branch survived because the grown chidren became

to a significant degree its support. Their duty - to repay the Home that had

helped them when in need - was spelled out in the magazine, and not only

donations but life insurance benefits were solicited by the Homes.

The magazine had years to instill the lesson in its readers, once the

pattern was established, if the youngsters followed the moral teaching of

the anecdotes selected by the editor as fit for printing. The 'need' for

life insurance, even for single men, labourers, just starting out in life,

was established in the readers by repetition of anecdotes of grown boys who

were dutifully repaying what the Home did for them by naming the Home as

beneficiary of whole-life policies.

So far as the insurance companies, Canada Life Assurance among them, were

concerned, Barnardo's Homes were a sales drive waiting to happen: imagine

the opportunity: one man, ABO speaks, and hundreds of his wards line up to

buy. The Institution bred children not only to become self-sufficient, but

also to become good providers in sustaining the work of the Home for the new

generation of immigrant children coming along.

=============================

After a few years of reading about the models presented as the ones to be

emulated, the younger children must have become thoroughly indoctrinated as

to the young adult that they were expected to become: pious, teetotaling and

non-smoking, thrifty savers, hard workers and self-teachers as well as good

students, sober obedient and, in addition, young adults mindful of what the

Homes have done to help them and willing to repay them through donations and

through life insurance benefits.

And it is my opinion that the practices of Barnardo's then, around the

pitching of whole-life policies to young adult men (who worked frequently at

dangerous occupations) has consequences to this day as to what information

Barnardo's Aftercare is willing to release about the brothers of our

Barnardo grandparents.

It is relevant to this question of life insurance that George Albertus Cox,

of Peterborough until ~1888, was president of Canada Life Assurance Company

for many years, and its Peterborough agent before that, from 1861 forward.

It is he who bestowed Hazel Brae on the Home. I have seen him described as

the richest Canadian west of Montreal; and that there is much mystery

surrounding his affairs because his family destroyed almost all of his

papers soon after his death in 1914.

Also of interest is that there was a Royal commission on Insurance in 1907,

and a Royal Commission on Business Practices in 1914, which apparently

resulted in the forced separation of banking, trust and insurance companies.

Brian Rolfe